United States, one of the largest feed and livestock industries in the world, has more than 5,800 animal feed manufacturing facilities and producing more than 284 million tons of finished feed and pet food each year. With this amount of feed production, the country follows China, which ranks first in world feed production with approximately 240 million tons. According to a market report, the US animal feed market size was about US$72.6 billion in 2018, and it is expected to reach US$83.6 billion in 2024, representing a steady CAGR of 2.4% over the 2019-2024 forecast period.

By Derya Yıldız

By Derya Yıldız

United States is one of the largest feed and livestock industries in the world. According to data of U.S. Department of Agriculture (USDA), livestock and poultry account for over half of U.S. agricultural cash receipts, often exceeding $100 billion per year.

Cattle production is the most important this industry in the U.S., consistently accounting for the largest share of total cash receipts for agricultural commodities. In 2021, cattle production is forecasted to represent about 17 percent of the $391 billion in total cash receipts for agricultural commodities. With rich agricultural land resources, the U.S. has developed a beef industry that is largely separate from its dairy sector. The country beef industry is unique when compared to countries like India that produce beef from water buffalo, which are used as dual-purpose animals. In addition to having the world’s largest fed-cattle industry, the U.S. is also the world’s largest consumer of beef—primarily high-value, grain-fed beef.

The cattle herd of the country, which decreased to 88.2 million heads in the beginning of 2014, started to increase again in the following years and reached its peak with 94.8 million heads in 2019. However, January 2021 data show that herd presence decreased by 1.3 percent to 93.6 million cattle.

Major trends in U.S. milk production include a fairly steady increase in milk production and a consistent decline in the number of dairy operations matched by a continual rise in the number of cows per operation. Milk is produced in all 50 states, with the highest producing states in the western and northern areas of the country. The top five milk production states in 2020 were California, Wisconsin, Idaho, New York, and Texas. These states collectively produced more than 50 percent of U.S. milk supply.

In the country, the decision to produce milk largely rests in the hands of individuals or families. Many of these farmers belong to producer-owned cooperatives. The cooperatives assemble members’ milk and move it to processors and manufacturers. Some cooperatives operate their own processing and manufacturing plants.

At the same time, the U.S. is the world’s third-largest producer and consumer of pork and pork products. In recent years, the country has been either the world’s largest or second largest exporter of pork and pork products, with exports averaging over 20 percent of commercial pork production in most years.

The U.S. hog industry has undergone significant structural changes in the last 40 years, the most of important of which has been the rapid shift to fewer and larger operations. Since 1990, the number of farms with hogs has declined by more than 70 percent, as individual enterprises have grown larger. U.S. hog operations tend to be heavily concentrated in the Midwest—Iowa and southern Minnesota particularly—and in eastern North Carolina, but hog operations are also found in Oklahoma and in Texas.

The U.S. poultry industry is the world’s largest producer and second largest exporter of poultry meat and a major egg producer. U.S. consumption of poultry meat (broilers, other chicken, and turkey) is considerably higher than beef or pork, but less than total red meat consumption. With almost 18 percent of total poultry production exported, the U.S. poultry industry is heavily influenced by currency fluctuations, trade negotiations, and economic growth in importing markets.

FEED AND FEED INGREDIENTS CONSUMPTION

According to a report published by The Institute for Feed Education and Research (IFEEDER); approximately 283.8 million tons of safe, high quality and nutritious food were fed to major species of livestock, poultry, aquaculture, and pets in 2019 with a value of $59.9 billion.

Working with the economic and analysis firm Decision Innovation Solutions (DIS), the study found that the top three feed consumers included beef cattle at 64.5 million tons, hogs at 61.8 million tons and broiler chickens at 60.8 million tons. Iowa, Texas, California, North Carolina and Minnesota topped the list for the sheer amount of animal food consumed with 28.8 million tons, 21.1 million tons, 17.5 million tons, 16.3 million tons and 14.6 million tons, respectively.

The prominent feed ingredient in US is corn. According to the IFEEDER report; corn, the most abundantly produced crop in the country, made up slightly more than half (52%) of the total amount of compounded feed consumed, and when combined with soybean meal (12%) and dried distillers’ grains with solubles (DDGs) (11%), represented more than 75% of all feed tonnage consumed in 2019.

The prominent feed ingredient in US is corn. According to the IFEEDER report; corn, the most abundantly produced crop in the country, made up slightly more than half (52%) of the total amount of compounded feed consumed, and when combined with soybean meal (12%) and dried distillers’ grains with solubles (DDGs) (11%), represented more than 75% of all feed tonnage consumed in 2019.

DIS also reported on a number of other ingredients used in animal diets, including wheat middlings and wheat bran (3%), animal byproduct meals (3%), corn gluten feed/meal (2%), canola meal (2%), animal fats (2%), other processed plant byproducts (1%) and others.

FEED MILLS AND FEED PRODUCTION

According to data from The American Feed Industry Association (AFIA), there are more than 5,800 animal feed manufacturing facilities in the U.S. producing more than 284 million tons of finished feed and pet food each year. The mill sizes vary tremendously from a small on-farm mixer to a modern, computerized system with few human operators making more than 1 million tons of feed each year for swine or poultry operations.

According to the Alltech Global Feed Survey 2021 report; there are around 6000 feed mills in the U.S. The annual total feed production of these mills, which was 214.4 million tons in 2019, increased by 1 percent in 2020 and reached 215.9 million tons. With this amount of feed production, the country follows China, which ranks first in world feed production with approximately 240 million tons. In short, the U.S., along with China, is by far one of the two largest feed producers in the world. Brazil, which is in the third place after the U.S. in the world ranking, produces almost 1/3 of the feed of these two countries (77.6 million tons).

Considering the feed production of the U.S. on the basis of species; it is seen that beef cattle feeds take the first place with 62,956 million tons. It is followed by broiler feeds with 47,797 million tons and pig feeds with 45,760 million tons. These three groups make up 72.5% of the total feed production in the country.

Among other feed types in the country, the production amount of dairy cow feeds is 24,100 million tons, the production amount of layer feeds is 13,650 million tons, the production amount of pets food is 8,709 million tons and the production amount of aqua feeds is around 0.910 million tons.

FEED MARKET SIZE, COVID-19 IMPACT AND FUTURE FORECASTS

FEED MARKET SIZE, COVID-19 IMPACT AND FUTURE FORECASTS

According to the market report of Research and Markets (2019-2024), the US animal feed market size was about US$72.6 billion in 2018, and it is expected to reach US$83.6 billion in 2024, representing a steady CAGR of 2.4% over the forecast period.

However, COVID-19 has caused some problems and changes in the feed industry like many other industries. The U.S. feed industry is no exception.

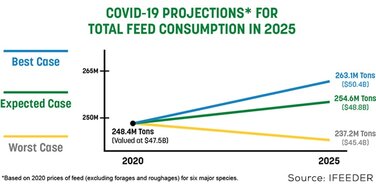

In the reoport of IFEEDER, DIS estimated the baseline consumption at the beginning of 2020 at 252.6 million tons (excluding forages and roughages) with an estimated value of $66.7 billion, under normal production circumstances without the pandemic; with COVID-19, the consumption rate fell roughly 1.7% to an estimated 248.4 million tons, a difference of 4.2 million tons less feed consumed worth $1.6 billion, leaving the industry with a total post-COVID-19 value of $47.5 billion.

According to the Research and Markets report, rising consumer awareness about the safety of animal products couple with outbursts of diseases in animals is the major factor contributing to the increasing demand for animal feed during the 2019-2024 forecast period. In addition, presence of major market players in the region is further expected to propel the market growth opportunities in the coming years. However, stringent regulatory structure about the animal feed production is expected to hinder the market opportunities in the coming years.

On the other hand, DIS makes its future predictions through three different scenarios in the IFEEDER report;

On the other hand, DIS makes its future predictions through three different scenarios in the IFEEDER report;

– In a worst-case scenario, where the industry encounters further disruptions in processing and slaughter numbers or potential trade issues, DIS estimated 2025 animal food consumption could further decrease 4.5% to 237.2 million tons at a value of $45.4 billion.

– In an expected-case scenario, where the industry continues business as usual without any further major disruptions, DIS estimated that by 2025 animal food consumption could increase 2.5% to 254.6 million tons worth roughly $48.8 billion.

– In a best-case scenario, where the hotel, retail and institution sectors of the economy recover quickly and travel and trade conditions dramatically improve, DIS estimated that by 2025 feed consumption could increase 5.9.% to 263.1 million tons, valued at $50.4 billion.

FEED INDUSTRY AND TRADE

The U.S. is also the world’s largest animal feed exporter, supplying a significant amount of the animal food for the livestock industries around the world. According to the trading data from ITC, the U.S. exported $2.8 billion worth of animal feed products to the global market in 2019, representing over 11% of the world’s total animal feed exports in that year. Some of the largest U.S. animal feed products importers were Canada, Mexico, Japan, China and Indonesia.

According to a study published in BizVibe; on a global landscape, the surging demand of livestock and livestock products, such as meat, dairy and eggs has spurred the growth of animal feed production and animal feed exports among many leading animal feed companies around the world. Today, the global animal feed production is estimated to be nearly 1 billion tonnes annually, while the world’s top 100 animal feed companies are responsible for about 42% of the world compound production volume every year. As the world’s largest animal feed market, the U.S. is also the home of many world’s leading animal feed producers.

According to a study published in BizVibe; on a global landscape, the surging demand of livestock and livestock products, such as meat, dairy and eggs has spurred the growth of animal feed production and animal feed exports among many leading animal feed companies around the world. Today, the global animal feed production is estimated to be nearly 1 billion tonnes annually, while the world’s top 100 animal feed companies are responsible for about 42% of the world compound production volume every year. As the world’s largest animal feed market, the U.S. is also the home of many world’s leading animal feed producers.

Again, according to the same study, as the U.S. remains the world’s largest animal feed producer and exporter in 2020, the top 10 largest animal feed manufacturers in the U.S. is expected to continue dominating the animal feed production and animal feed exports in the global market.

Resources:

1. The Institute for Feed Education and Research (IFEEDER) and Decision Innovation Solutions (DIS), Animal Feed/Food Consumption and COVID-19 Impact Analysis, December 2020,

2. The American Feed Industry Association (AFIA), Feed Industry Statistics,

3. U.S. Department of Agriculture (USDA), Animal Products,

4. Alltech Global Feed Survey 2021,

5. BizVibe, The US Animal Feed Industry Factsheet 2020: Largest Animal Feed Manufacturers in the US & the World, 1 April 2021,

6. Research and Markets, United States Animal Feed Market – Forecasts from 2019 to 2024,