Global aquaculture markets entered 2026 with resilient demand supporting prices across key species, despite ongoing geopolitical uncertainty. According to a new RaboResearch report, tight supply conditions, shifting trade flows, and climate risks continue to shape market dynamics.

Resilient demand continues to underpin prices across key species, even as tight supply conditions, shifting trade flows, and ongoing geopolitical uncertainty shape global seafood markets in early 2026, according to a new RaboResearch report.

Resilient demand continues to underpin prices across key species, even as tight supply conditions, shifting trade flows, and ongoing geopolitical uncertainty shape global seafood markets in early 2026, according to a new RaboResearch report.

GLOBAL TENSIONS RESHAPE TRADE FLOWS

Global seafood markets enter 2026 on a cautiously optimistic footing, as steady demand in key markets contrasts with a supply landscape shaped by shifting trade flows and lingering geopolitical uncertainty. “While inflation has eased in major economies, supporting demand, the industry still faces headwinds from macroeconomic uncertainty, evolving tariff regimes, and climate‑related pressures,” says Novel Sharma, Seafood analyst at RaboResearch.

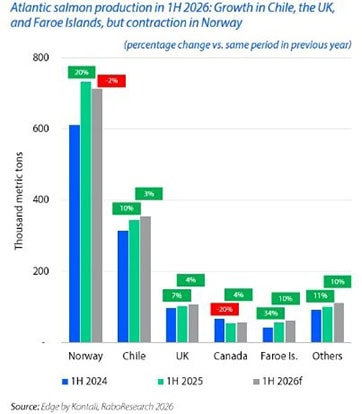

SALMON: SUPPLY GROWTH SET TO STALL IN EARLY 2026

SALMON: SUPPLY GROWTH SET TO STALL IN EARLY 2026

Global salmon output is expected to rise by just 0% to 2% in the first half of the year. Norway, the world’s largest producer, and Chile, the second‑largest, both enter 2026 with constrained biomass following strong late‑2025 harvesting, according to Sharma. “The heavy harvesting at the end of 2025 really reduced biomass levels, so we’re only expecting very modest, low single‑digit growth in early 2026. That said, there is still some upside if biological conditions turn out as favorable as they were early last year. We’re already seeing tighter supply push prices higher, with a clear rebound underway in both Europe and the US. And despite the broader economic headwinds, global demand has held up remarkably well – salmon continues to offer great value for consumers across Europe, Asia, and Latin America,” he adds.

SHRIMP: TARIFF EXPOSURE AND MARKET ACCESS DEFINE COMPETITION

“In the US, we saw shrimp imports ease toward the end of 2025 as buyers worked through the extra product they had brought in ahead of the tariffs,” says Sharma. “That’s likely to keep shipments softer in early 2026. Europe was able to take on some of the volumes diverted from the US, but late‑year stock‑building could limit how much more the region can absorb. In China, imports settled into a more normal pattern by mid‑2025 before easing again later in the year. Prices have stayed fairly steady, which tells us demand is healthier than the headline volumes might suggest, even with economic uncertainty and more domestic production coming online.” He points out that, competitively, tariffs and market access are playing an even bigger role: Ecuador continues to benefit from tariff advantages and growing value‑added capacity; India is under pressure as US duties squeeze margins; Vietnam holds its ground in higher‑value segments; and Indonesia remains challenged by its reliance on the US and rising competition in the region.

FISH MEAL: TIGHT SUPPLY KEEPS PRICES HIGH

Global fish meal markets head into 1H 2026 under tight supply conditions, shaped by Peru’s challenging 2025 anchovy season. “The second season opened with a provisional quota of just 500,000 metric tons because unusually warm surface waters had pushed anchovy schools deeper than normal, making early biomass estimates difficult. As more surveys came in, the picture improved, and the biomass was revised up to 5.6 million metric tons. That allowed the quota to be raised to 1.6 million metric tons, although that’s still the lowest level we’ve seen since 2017, when El Niño had a major impact on the fishery. Looking ahead, there’s a good chance we’ll move back toward ENSO‑neutral conditions in early 2026. If ocean temperatures return to something closer to normal, that should give the biomass some room to recover, but there are still risks if surface temperatures fluctuate,” he warns. “Even if supply does improve, we expect fish meal prices to stay elevated.”