Global seafood trade is being disrupted by tariffs, sanctions, and shifting alliances, hitting Asian exporters and causing price volatility and reduced availability for consumers in the US and Europe, a recent RaboResearch report reveals.

The global seafood industry is facing a period of profound disruption, as geopolitical tensions and trade interventions reshape long-established supply chains, according to a recent RaboResearch report. Seafood producers and exporters – particularly in Asia – are being hit hard by tariffs, sanctions, and shifting alliances, while consumers in the US and Europe face rising prices and reduced availability of seafood staples.

UNPRECEDENTED TRADE TURBULENCE

The report reveals that the seafood industry – one of the most globally traded food sectors – is facing unprecedented trade turbulence. While some markets may eventually stabilize, the uncertainty surrounding trade policy is already deterring investment and undermining long-term planning. Domestic market development may offer a partial buffer, but the path forward remains complex.

“The seafood industry is navigating a perfect storm of trade barriers, geopolitical risk, and supply chain fragility,” says Gorjan Nikolik, Senior Global Specialist Seafood at RaboResearch. “Strategic diversification—both in sourcing and market access—is no longer optional. It’s essential.”

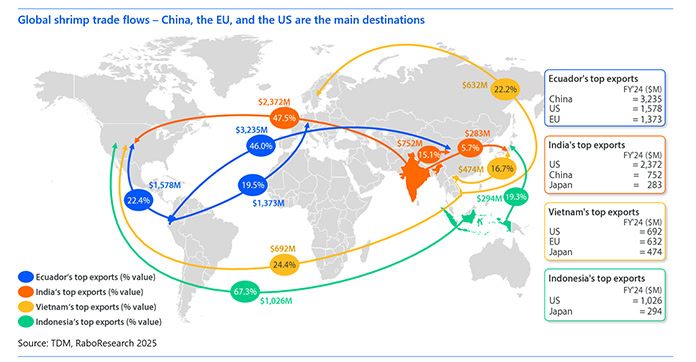

THE SHRIMP SECTOR FACES ACUTE DISRUPTION FROM U.S.

US tariffs of up to 50% are disproportionately affecting Asian exporters, including India, Vietnam, and Indonesia. In the US, shrimp is the most consumed seafood, making it a critical import market. Given the improbability of passing on tariffs exceeding 40% to consumers, a decline in US shrimp consumption appears inevitable, analysts predict.

According to Nikolik, as trade flows are rerouted, oversupply in alternative markets is triggering global price volatility. These deteriorating market conditions will test the resilience of producers and expose structural vulnerabilities in the sector’s reliance on a few key markets.

According to Nikolik, as trade flows are rerouted, oversupply in alternative markets is triggering global price volatility. These deteriorating market conditions will test the resilience of producers and expose structural vulnerabilities in the sector’s reliance on a few key markets.

SALMON INDUSTRY WILL STRUGGLE TO ADAPT

Potential US tariffs on Canadian salmon – currently under discussion – could destabilize a market where 87% of Canadian exports go to the US. The threat alone of 25% to 35% tariffs is already stalling investment, and consumers could face higher prices and reduced supply. Unlike shrimp, salmon has low supply elasticity. The production cycle spans nearly three years, and regulatory hurdles make rapid expansion virtually impossible. As a result, the only short-term levers are trade reallocation and price adjustments.

CHINESE OVERSUPPLY OF TILAPIA COULD DEPRESS PRICES IN AFRICA AND LATIN AMERICA

Chinese tilapia now faces a 75% US tariff, making it uncompetitive. With few viable substitutes, US consumption is expected to fall sharply. The repercussions of this contraction will extend beyond the US market. “We expect Chinese producers to redirect supply to domestic consumers or to alternative markets such as sub-Saharan Africa and Mexico,” adds Nikolik. However, these regions already have established local industries, and without protective tariffs, they may be vulnerable to a flood of low-cost imports.

TRADE RESTRICTIONS ON RUSSIAN-ORIGIN FISH HAVE HAD GLOBAL IMPACT

Russian-origin fish, once central to global supply of groundfish, is extremely restricted. The EU and UK have imposed tariffs, while the US has enacted a full ban. Analysts report that the resulting price inflation has placed significant strain on seafood processors and foodservice operators, particularly in the UK, where the decline of fish and chip shops has accelerated. Rerouted Russian groundfish has been flooding Asian markets in the form of surimi, squeezing producers across the value chain.