At the heart of the global feed and livestock industry, China is undergoing a profound transformation during the 2024-2025 period, focused on efficiency, sustainability, and reducing foreign dependency. The structural changes in animal protein production, the compound feed market, raw material composition, and additives are reshaping global commodity balances and sectoral strategies.

By Derya Gulsoy Yildiz

China stands as the epicenter of the global livestock and feed industry. Rapidly increasing demand for protein driven by economic prosperity, together with urbanization and shifting dietary habits have transformed the country into a massive compound feed market. In China, which maintains its leadership in global compound feed production according to 2024 data, the feed sector is undergoing a fundamental transformation driven by state policies aimed at increasing efficiency, ensuring sustainability, and reducing foreign dependency.

LIVESTOCK SECTOR AND ANIMAL PROTEIN CONSUMPTION

Although China’s livestock economy has historically been structured around pork, shifting modern consumer preferences are driving an increased demand for beef, poultry, and seafood. According to data from Rabobank, per capita meat consumption in the country—which stood at 35 kilograms in the mid-1990s—has more than doubled, reaching 72 kilograms as of 2023. National Bureau of Statistics of China also indicates that total red meat and poultry production reached 96.63 million tons in 2024, representing a 0.2% increase. This explosion in demand has facilitated the livestock sector’s transformation from traditional, small-scale “backyard” farming into massive, technology-driven, and capital-intensive industrial complexes with vertical integration.

Pork and the Swine Sector

Pork is the absolute dominant force in China’s food security and agricultural economy. The country alone accounts for approximately 50% of global pork consumption. However, 2024 has been a challenging period for the sector. Following three years of steady growth, pork production fell for the first time in 2024, decreasing by 1.5% to 57.06 million tons.

The deep financial losses experienced in 2023 and the disease outbreaks seen at the end of the year are cited as the primary reasons behind this contraction in the sector. According to the USDA’s report titled Livestock and Products Semi-Annual, Chinese pork producers recorded their largest annual losses since 2014 in 2023. This situation led to the liquidation of herds and a planned reduction in the breeding sow inventory in 2024.

Beef and Dairy Sector

In China, the beef and dairy sectors are highly interconnected, in contrast to the U.S. model. In 2024, beef production increased by 3.5% to reach 7.79 million tonnes. However, this increase does not reflect healthy sector growth; rather, it is driven by the diversion of female cattle and dairy cows into the beef market due to the ongoing crisis in the dairy sector.

The dairy sector entered a “production at a loss” period in 2024. Continuous declines in raw milk prices combined with weak domestic consumption have caused more than 80% of dairy farming enterprises to operate at a loss. This economic pressure has led to the early slaughter of dairy cows, creating deflationary pressure on beef prices. To stabilize beef and mutton production, the Chinese Ministry of Agriculture and Rural Affairs (MARA) has announced subsidies for feed conversion and quality improvement projects.

In terms of live cattle imports, a dramatic decline was observed at the beginning of 2025. In the first five months of 2025, live cattle imports fell by 65% compared to the same period of the previous year, dropping to 14,000 head. This situation reflects the extremely cautious approach of domestic producers toward new investments and capacity expansion.

Poultry Sector

The poultry sector was the most resilient and fastest-growing segment of Chinese livestock in 2024. According to data from the National Bureau of Statistics, total poultry meat production rose by 3.8% to 26.6 million tons. The primary driver of this growth is the emergence of chicken as a more economical and “budget-friendly” protein option compared to pork and beef.

The number of broilers slaughtered in 2024 broke a historical record, reaching 13.56 billion head. In particular, white-feathered broilers (up 2.77%) and yellow-feathered broilers (up 3.26%) were driving force behind the market. On the egg production side, the sector has reached a saturation point; while small-scale breeders are being phased out, the number of modern, high-capacity facilities housing millions of birds is increasing rapidly. The poultry sector is one of the segments with the highest integration rate, which directly supports professional feed consumption.

Aquaculture

China stands as the undisputed global leader in the production, consumption, and trade of aquatic products. The years 2024 and 2025 represent a critical threshold in the sector’s transition from traditional methods to a technology-intensive, sustainable, and efficiency-oriented structure. The sector plays a central role not only in terms of food security but also in rural development, technological innovation, and maritime economy strategies. As of 2024, China maintained its title as the world’s largest producer of aquatic products, with total production reaching 74.1 million metric tons. This volume represents a 4% increase compared to 2023, and the main driver of growth is aquaculture activities, which account for more than 80% of total production (60.8 million metric tons).

The increase in disposable income across the country is shifting consumption habits away from basic protein sources toward high-quality, value-added products. As of 2024, seafood consumption in China is growing faster than meat consumption. According to OECD-FAO projections, per capita seafood consumption in China is expected to increase by 14% by 2032.

Top 10 Feed Producers in China

1. New Hope Group

2. Wen’s Foodstuff Group

3. CP Group (Charoen Pokphand)

4. Haid Group

5. Twins Group

6. Tongwei Group

7. Cargill (China)

8. COFCO

9. CJ Tianjin Feed

10. TRS Group (Tech-bank)

INDUSTRIAL FEED PRODUCTION AND CONSUMPTION IN CHINA

As the world’s largest feed producer, China represents a remarkable market in terms of the animal nutrition sector. According to the report titled 2025 Agri-Food Outlook prepared by Alltech, in 2024, when global feed production reached approximately 1.396 billion metric tons, China’s feed production declined slightly by 2.03% compared to the previous year, falling to 315.030 million metric tons. Oversupply, low prices, and disease outbreaks caused a decline in the use of swine, beef, dairy, and aquafeeds across the country, resulting in a minor reduction in total compound feed production. Despite this decline, China maintains its global leadership in feed production with a massive volume of 315 million metric tons, surpassing its closest competitor, the United States (approximately 270 million tons). The country controls more than 22.5% of global feed production on its own and produces more than the combined output of other major producers such as Brazil and India.

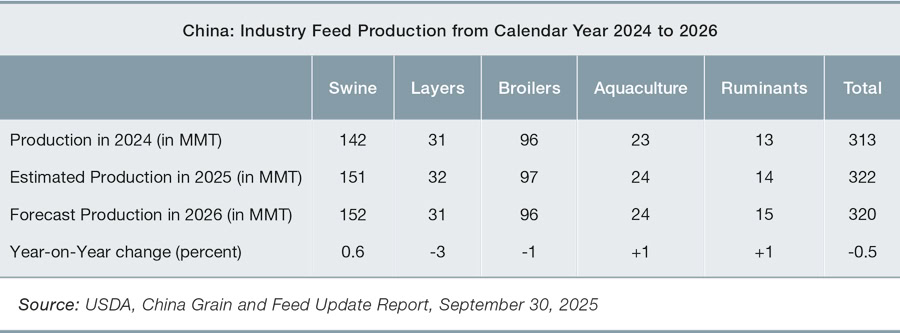

Swine feed is the backbone of China’s compound feed production, representing approximately 47% of total output. Swine feed production, which reached a record level of 149.75 million metric tons in 2023, came under pressure in 2024 due to severe losses in the livestock sector and capacity reduction processes. In the first half of the same year, a 6% decline was observed in swine feed consumption, which remained at 142 million metric tons. The USDA estimates that swine feed consumption increased again in 2025, reaching a level of 146 million metric tons.

Poultry feed is the second-largest segment, representing 40% of feed production in China. Within the poultry group, broiler feed production recorded a 1.8% growth in 2024, as consumers turned to chicken—a more affordable protein source—due to rising red meat prices. The USDA predicts that broiler feed consumption, which was around 96 million metric tons in 2024, will exceed 97 million metric tons in 2025. The layer feed segment presents a more complex picture compared to the broiler segment. USDA analysts estimate that layer feed consumption, which stood at 32.7 million metric tons in 2024, will reach levels of 32.9 million tons in 2025, representing a 0.6% increase.

As the world’s largest producer of aquatic products, China also stands out in the consumption of aquafeed, in direct proportion to its production volume. However, the 2023-2024 period saw a contraction in aquafeed production due to falling fish prices and disease outbreaks. According to USDA data, the country’s aquafeed consumption in 2024 was approximately 21.9 million metric tons. Forecasts indicate that consumption will increase by 2.2% in 2025, reaching around 22.5 million metric tons. As a sub-segment, freshwater fish account for more than 80% of the aquafeed market.

China’s ruminant feed production represents approximately 5% of the total market and stood at 16.7 million metric tons in 2023. Production and consumption are showing a decline, particularly due to problems in the dairy farming sector. According to USDA data, total ruminant feed consumption fell to 15.4 million metric tons in 2024. It is estimated that this decline continued into 2025, with consumption hovering around 15.3 million metric tons, representing a 0.5% decrease.

Pet food is the fastest-growing and most profitable niche area of the Chinese feed sector. In 2024, China’s total pet food production increased by 9.3%, reaching 1.6 million tons. This segment continues to move in a positive direction despite the contraction in the overall feed sector.

A NEW ERA IN FEED RAW MATERIALS

A NEW ERA IN FEED RAW MATERIALS

The massive scale of China’s feed sector is directly linked to the country’s food security policies. The raw material composition of feed in the country is largely based on corn and soybean meal. However, in line with the goals of reducing geopolitical risks and foreign dependency, a revolutionary change is taking place in ration structures.

The Beijing administration has adopted the “Dual Circulation” strategy, which aims to reduce foreign dependency and optimize domestic production, particularly in key inputs such as corn and soybean meal. This strategy is supported by concrete action plans, such as lowering the ratio of soybean meal in feed rations and increasing domestic corn production.

Corn and Energy Sources

Corn is the cornerstone of China’s feed rations. For the 2024/25 marketing year, corn production is expected to break a record, reaching 294.9 million metric tons due to an increase in planted areas and the use of high-yield varieties. Low corn prices have allowed feed mills to increase the proportion of corn in their rations, which in turn has reduced the share of alternatives such as wheat and old-stock rice in the feed.

China is also promoting the use of genetically modified seeds and “grain-to-feed” projects to increase self-sufficiency in corn production. In the 2025/26 period, corn is expected to maintain its dominant position in feed rations, thereby suppressing the need for imported raw materials.

Soybean Meal Reduction Strategy

China imports approximately 100 million tons of soybeans annually, with over 90% of this demand met by Brazil and the United States. This massive dependency is considered a strategic risk in terms of food security. In response, MARA implemented the “Three-Year Action Plan for Reducing Soybean Meal Consumption” in 2023.

The primary goals of the action plan are:

• Inclusion Rate: Reducing the soybean meal ratio—which was 17% in 2017—to below 13% by 2025 and to 10% by 2030.

• Mechanism: Supplementing low-protein diets with synthetic amino acids (lysine, methionine, threonine).

• Alternatives: Expanding the use of protein sources such as rapeseed, cottonseed, peanut meal, and food waste.

According to official data, the soybean meal inclusion rate was reduced to below 13% in 2023, resulting in a saving of 9 million tons in soybean demand. However, the USDA and some independent analysts suggest that this decline is occurring more slowly than official figures claim, as low soybean prices incentivize producers to use more soybeans.

FEED ADDITIVES AND MICRO-NUTRITION

The 2020 ban on antibiotic growth promoters (AGPs) has pushed the Chinese feed sector toward a biotechnology-oriented transformation. The market’s focus has shifted to functional additives that enhance productivity while protecting animal health. In 2024, the production value of China’s feed additives increased by 7.5%, reaching 131.58 billion yuan (approximately 18.4 billion USD).

In particular, the production of amino acids such as lysine, methionine, and threonine showed a 21.7% increase. This growth stems from the supplementation of low-protein rations (the soy reduction policy) with synthetic amino acids. On the enzyme side, enzymes that enhance carbohydrate digestion maintain their leadership with a 46% share, while the phytase enzyme is rapidly becoming widespread to reduce phosphorus pollution and increase feed efficiency.

FEED MILLS AND PRODUCTION INFRASTRUCTURE

China possesses one of the world’s most advanced feed infrastructures, not only in terms of quantity but also in regarding facility modernization. The sector is evolving from small, inefficient mills into massive, fully automated, and digitally controlled facilities with annual capacities exceeding millions of tons.

As of 2024, industrial feed production in China is concentrated in the Shandong and Guangdong provinces. Each of these two provinces produces over 30 million tons annually. Other strategic production hubs exceeding the 10-million-ton threshold include provinces such as Jiangsu, Guangxi, Sichuan, and Henan.

In 2024, China’s feed infrastructure expanded with 475 new modern feed mills. These investments aim to decommission facilities using outdated technology and replace them with high-capacity, energy-efficient, and environmentally friendly plants. Notably, 49.2% of industrial feed production is delivered as bulk feed, which significantly reduces packaging and logistics costs.

CONCLUSION AND STRATEGIC OUTLOOK

The livestock and feed sectors of the People’s Republic of China are undergoing a process of “transition and consolidation” during the 2024–2025 period. The era of rapid expansion has been replaced by a structure focused on efficiency, digitalization, and reducing foreign dependency. The most significant transformation within the sector is the systematic reduction in the use of soybean meal and the optimization of rations through synthetic amino acids and enzymes.

In the coming decade, the engine of growth in the Chinese feed market will no longer be volume expansion, but rather the increase in value-add. Pet food, smart feeding technologies, and antibiotic-alternative additives are emerging as the most attractive areas for global suppliers and investors. The deepening vertical integration of Chinese giants is making the sector more resilient to fluctuations in raw material markets, while also indicating that China’s influence on global commodity prices will continue to grow.

References:

1. 2025 Agri‑Food Outlook Report | Global Feed Production Trends & Insights I Alltech

2. Animal feed preparations nes in China Trade | The Observatory of Economic Complexity

3. Aquaculture Industry Composition, Distribution, and Development in China I MDPI

4. Brazilian soybeans and China’s food security | The Strategist

5. Can China Reduce Soybean Import Demand? Evaluating Soybean Meal Reduction Efforts – farmdoc daily I Jilang Qing and Joe Janzen, Department of Agricultural and Consumer Economics, University of Illinois

6. China 2024 pork output falls for first time in four years | The Pig Site

7. China Animal Feed Industry Outlook 2024 – 2028 I ReportLinker

8. China Animal Feed Market By Size, Share and Forecast 2030F | TechSci Research

9. China Animal Feed Market Size, Trends & Forecast Report 2031 I GMI Research

10. China Animal Feed Market Size, Trends and Forecast to 2032 I DataBridge

11. China Animal Feed Market, By Region, Competition, Forecast & Opportunities, 2020-2030F I Research and Markets

12. China Aquafeed Market – Manufacturers, Suppliers & Industry Analysis I Mordor Intelligence

13. China Compound Feed Market Size & Share Outlook to 2030 I Mordor Intelligence

14. China Feed Additives Market Share & Size 2030 Outlook I Mordor Intelligence

15. China Fishery Products, Grain and Feed Annual, Grain and Feed Update, Livestock and Products Annual, Pet Food Market Update Reports I Browse Data and Analysis | USDA Foreign Agricultural Service

16. China Pet Food & Animal Feeds Market 2024 I Euromonitor International I Scribd

17. China’s production of cattle, sheep, poultry remains stable in 2024 I The State Council, The People’s Republic of China

18. Could China’s Soy Policy Changes Drive a Sustainable Agricultural Transformation? | The FAIRR Initiative

19. A review of China’s feed production in 2023 I eFeedLink

20. Characteristics and implications of changes in China’s feed industry in 2024 I eFeedLink

21. Sector Trend Analysis – Fish and seafood trends in China I Agriculture and Agri-Food Canada (AAFC)

22. The changing face of China’s animal protein market – four key trends set to shape future of consumption I Rabobank

23. Tighter times ahead for the soybean market | ING Think

24. Top 10 Animal Feed Manufacturers in China ı Knowlege I CJ (Tianjin) Feed Co., Ltd