Global oilseed supply and demand points to strong production and consumption across all major product groups, particularly soybeans, rapeseed, sunflower seeds, palm kernel and cottonseed, as we enter the 2025/26 season. While demand growth driven by feed, oil and industrial uses continues to be noteworthy, trade-related shifts in some countries are creating sensitive points in the market.

By Derya Gulsoy Yildiz

The 2024/25 season saw a generally stable production and trade structure in the global oilseed complex. However, new season projections shared by the United States Department of Agriculture Foreign Agricultural Service (USDA FAS) indicate that growth expectations for both production and consumption in the oilseed market are continuing in the 2025/26 season.

OILSEED PRODUCTION: 2024/25 SEASON AND 2025/26 OUTLOOK

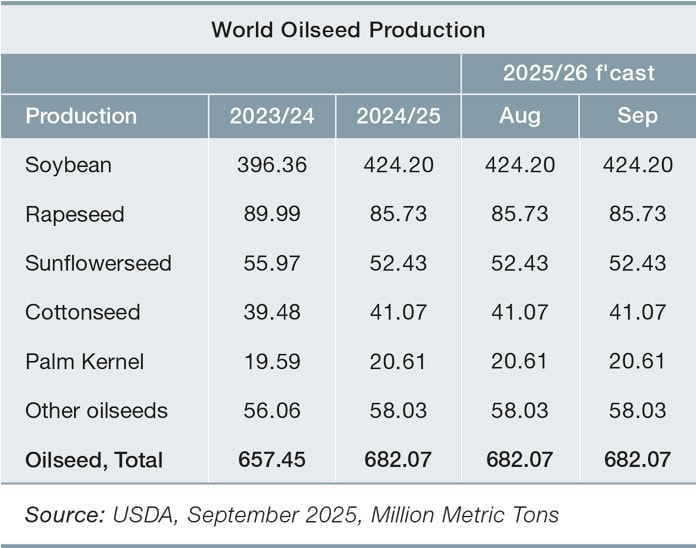

According to USDA data from September 2025, global oilseed production, which stood at 682.1 million tons in the 2024/25 season, is expected to reach 691.6 million tons in the 2025/26 season. This estimated figure is approximately 9.5 million tons higher than the previous season and indicates a strong increase in production. According to estimates for the 2025/26 season, soybeans account for the largest share of global oilseed production at 61.6%. Soybeans are followed by rapeseed at 13.2%, sunflower seeds at 8%, cottonseed at 6% and palm kernel at 3%. These five oilseed types account for 91.8% of global oilseed production. Production of other oilseeds is around 58 million tons.

Brazil has the largest share of oilseed production on a country basis. According to USDA data, Brazil will produce 182.5 million tons of oilseeds in the 2025/26 season. This expectation indicates an increase of 6.4 million tons compared to the previous season. In global oilseed production for the 2025/26 season, Brazil will be followed by the United States with 126.8 million tons, China with 68.8 million tons, Argentina with 54.8 million tons, and India with 42.3 million tons.

Soybean

Soybean

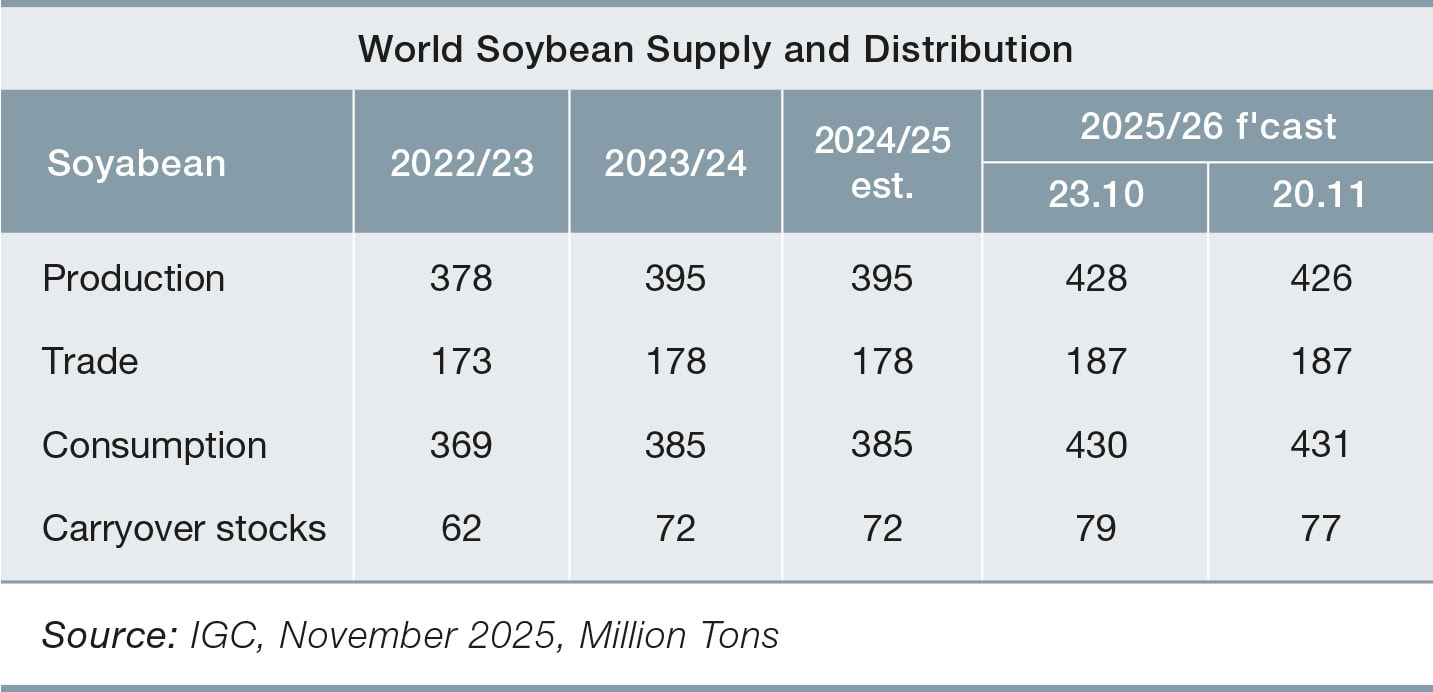

Soybean, the most important feed component in the animal feed sector, continue to be the backbone of global oilseed production. According to USDA data, soybean production, which was approximately 424.2 million tons in the 2024/25 season, is expected to reach 425.9 million tons in the 2025/26 season, an increase of 1.7 million tons. However, the latest report from the International Grains Council (IGC) indicates that soybean production will decline. According to IGC data from November 2025, global soybean production, estimated at 429 million tons in the 2024/25 season, will decline by approximately 3 million tons to around 426 million tons in the 2025/26 season.

According to the USDA’s 2025/26 estimates, Brazil will maintain its position as the world’s largest soybean producer with an estimated output of approximately 175 million tons. Although a slight decline is expected in the United States and Argentina due to weather conditions and changes in planting areas, total soybean production remains strong. The United States is expected to produce 117 million tons of soybeans in the 2025/26 season, while Argentina is expected to produce 48.5 million tons. China and India are the other two major producers contributing to soybean production. China’s production is forecast to be around 21 million tons in the 2025/26 season, while India’s production is expected to be around 11.6 million tons.

Of the 425.9 million tons of soybeans produced in the 2025/26 season, 287.7 million tons are expected to be marketed as soybean meal. When it comes to soybean meal production, the global producer ranking changes, with China taking the top spot. According to the USDA’s 2025/26 season estimates, China’s soybean meal production will be around 85.5 million tons in 2025/26. China will be followed by the United States with 54.6 million tons, Brazil with 44.8 million tons and Argentina with 33 million tons in soybean meal production.

Rapeseed

Rapeseed stands out as the second most widely produced oilseed globally. Global rapeseed production, which reached 85.7 million tons in the 2024/25 season, is expected to increase by 5.3 million tons to approximately 91 million tons in the 2025/26 season, according to USDA estimates. This represents the largest expected production increase among all oilseed types. Canada leads rapeseed production with 20 million tons. It is followed by the EU with 19.7 million tons, China with 15.9 million tons, and India with 12 million tons.

In the 2025/26 season, approximately 49.6 million tons of the 91 million tons of rapeseed production are expected to be marketed as rapeseed meal. The EU, China, Canada and India stand out with their strong performance in rapeseed meal production, as they do in rapeseed production. In the 2025/26 season, the EU is expected to produce 14 million tons, China 11.5 million tons, Canada 6.5 million tons and India 6.4 million tons of rapeseed meal.

Sunflower Seed

According to USDA data, global sunflower seed production reached 52.4 million tons in the 2024/25 season. Expectations for the 2025/26 season are that production will increase by approximately 2.9 million tons to reach 55.3 million tons. Russia has the largest share in global sunflower seed production and is expected to produce 19 million tons of sunflower seeds in the 2025/26 season. Russia is followed by Ukraine with 12.7 million tons and the EU with 8.9 million tons.

Of the global sunflower seed production, which is expected to reach 55.3 million tons in the 2025/26 season, approximately 22.4 million tons are expected to be marketed as sunflower meal. Russia is expected to account for the largest share of sunflower meal production during this period, with 7.4 million tons. Ukraine will follow Russia in sunflower meal production with 5.1 million tons, and the EU will follow with 4.4 million tons.

Cottonseed and Palm Kernel

According to USDA data, cottonseed production, which was 41 million tons in the 2024/25 season, will decline by approximately 200,000 tons to 40.8 million tons in the 2025/26 season. Global palm kernel production, announced at 20.6 million tons for the 2024/25 season, will reach 21.6 million tons in the 2025/26 season.

OILSEED CONSUMPTION: 2024/25 SEASON AND 2025/26 OUTLOOK

OILSEED CONSUMPTION: 2024/25 SEASON AND 2025/26 OUTLOOK

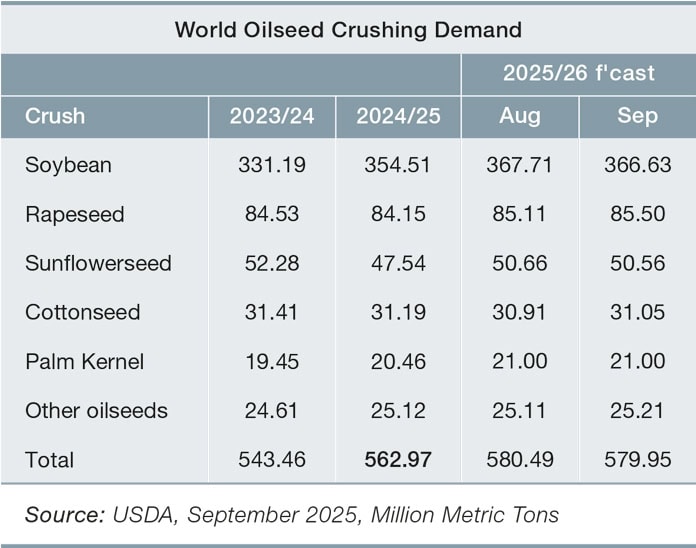

Global oilseed consumption is expected to remain strong in the new season for feed, oil and industrial use. According to the USDA, global oilseed crushing consumption volume reached approximately 563 million tons in the 2024/25 season. This volume is expected to increase by 17 million tons to approximately 580 million tons in the 2025/26 season. This figure indicates an increase in both feed protein requirements and vegetable oil demand. Soybeans account for the largest share of oilseed crush at 63.2%, which is directly proportional to their production volume. They are followed by rapeseed at 14.7%, sunflower seeds at 8.7%, cottonseed at 5.4%, and palm kernel at 3.6%. According to forecasts for the 2025/26 season, China will have the largest share of global oilseed crushing at 146.2 million tons. It will be followed by the United States with 73.7 million tons, Brazil with 64.1 million tons, the EU with 48.2 million tons, and Argentina with 46.7 million tons.

Data on oilseed meal consumption points to a significant increase. According to USDA data, total oilseed meal consumption, which was around 380.5 million tons in the 2024/25 season, will reach 395.3 million tons in the 2025/26 season. Soybean meal accounts for approximately 283.9 million tons of this consumption, while rapeseed meal accounts for 49.2 million tons. China accounts for the largest share of oilseed meal consumption at 113 million tons. It is followed by the EU with 51.4 million tons, the US with 43.9 million tons and Brazil with 24.4 million tons.

Soybean

Soybean

Soybean meal and oil production continues to be the main determinant of demand in the feed sector. According to USDA data, the amount of soybean crushing, which was around 354.5 million tons in the 2024/25 season, is expected to reach 366.6 million tons in the 2025/26 season, an increase of approximately 12 million tons. The IGC, which reports total consumption data, forecasts that total soybean consumption, estimated at 419 million tons in the 2024/25 season, will reach 431 million tons in the 2025/26 season, a record increase of 12 million tons. According to the IGC, this increase in consumption will cause carryover stocks to fall from 82 million tons in the 2024/25 season to 77 million tons.

China has the largest share of global soybean crushing on a country basis. According to USDA estimates, China will process 108 million tons of soybeans in the 2025/26 season. It will be followed by the US with 69.5 million tons, Brazil with 58 million tons, Argentina with 42.4 million tons, the EU with 15.3 million tons and India with 10.3 million tons.

A similar picture can be seen in soybean meal consumption. According to USDA estimates, China alone will account for 84.2 million tons of the 283.9 million tons of soybean meal consumption in the 2025/26 season. The United States will follow China in soybean meal consumption with 37.8 million tons, the EU with 29.2 million tons, and Brazil with 21.5 million tons.

Rapeseed and Sunflower Seed

Rapeseed crushing is expected to increase by around 1.3 million tons. According to USDA data, rapeseed crushing volume, which was 84.2 million tons in the 2024/25 season, will be around 85.5 million tons in the 2025/26 season. Rapeseed meal consumption will be 49.2 million tons during the same period. China and the EU will lead rapeseed meal consumption with 14 million tons each.

Approximately a 3 million ton increase is expected in sunflower seed crushing. According to the data, sunflower crushing volume, which was 47.5 million tons in the 2024/25 season, will reach 50.6 million tons in the 2025/26 season. Sunflower meal consumption is also expected to reach 22.1 million tons in the same season. The EU will account for the largest share of this consumption with 6.2 million tons, followed by Russia with 4.4 million tons.

Cottonseed and Palm Kernel

Global demand for cottonseed will decline. According to USDA data, the cottonseed crushing rate, which was around 31.2 million tons in the 2024/25 season, will decline to 31.1 million tons in the 2025/26 season. During the same period, consumption of cottonseed meal is expected to remain limited to 14.2 million tons.

In palm kernel, demand is expected to remain almost unchanged with minimal increase. According to USDA data, the palm kernel crushing volume, which was 20.5 million tons in the 2024/25 season, will be around 21 million tons in the 2025/26 season. Palm kernel meal consumption is forecast to be 10.6 million tons in the same season.

OILSEED TRADE: 2024/25 SEASON AND 2025/26 OUTLOOK

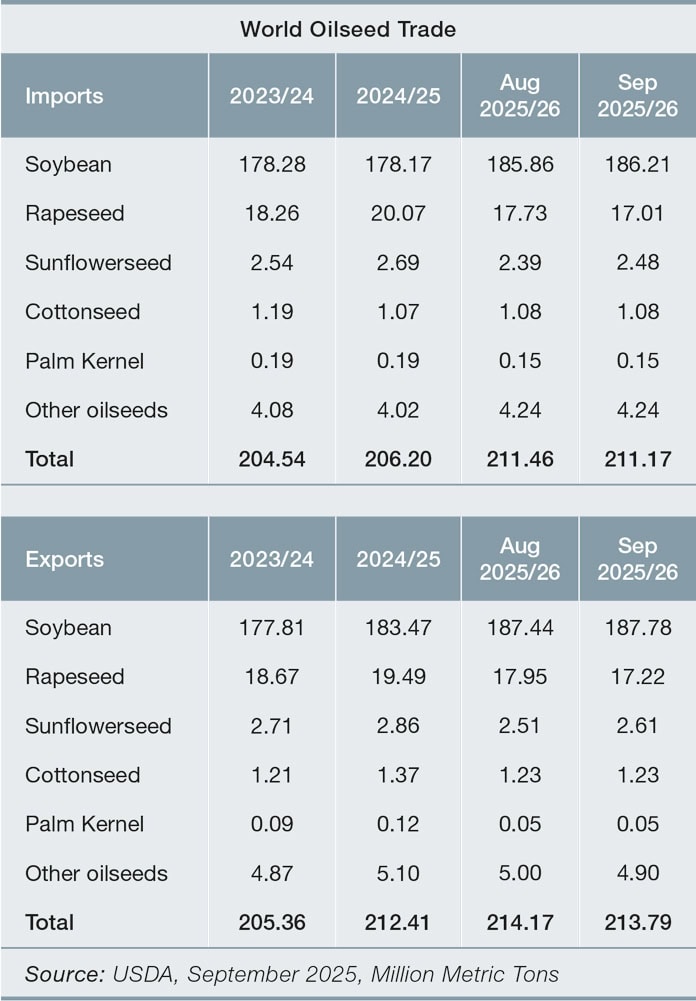

Global oilseed trade continues to expand overall in the 2025/26 season, despite some vulnerabilities. According to USDA data, oilseed imports, which stood at 206.2 million tons in the 2024/25 season, will reach 211.2 million tons in 2025/26 season. Soya beans (186.2 million tons) account for 88.2% of global oilseed imports, while rapeseed (17 million tons) accounts for 8%.

China has the largest share of oilseed imports on a country basis, and is expected to import approximately 117.5 million tons of oilseeds in the 2025/26 season. Approximately 112 million tons of this will be soybean imports and 4.1 million tons will be rapeseed imports. The EU follows China with 21.7 million tons of oilseed imports. Of the EU countries’ oilseed imports, the largest share is soybeans with 14.3 million tons and rapeseed with 5.7 million tons. These countries are followed by Mexico with 8.1 million tons of oilseed imports (6.7 million tons of soybean imports) and Argentina with 7.2 million tons of oilseed imports (all of which are soybean imports).

Brazil has the largest share in global oilseed exports. According to USDA estimates, Brazil will export 112.6 million tons of oilseeds in the 2025/26 season, almost all of which will be soybeans. Brazil will be followed in oilseed exports by the United States with 46.9 million tons (45.9 million tons of soybean exports) and Canada with 11.8 million tons (5.1 million tons of soybean exports and 6.7 million tons of rapeseed exports).

OILSEED MEAL TRADE: 2024/25 SEASON AND 2025/26 OUTLOOK

OILSEED MEAL TRADE: 2024/25 SEASON AND 2025/26 OUTLOOK

Oilseed meal trade is expected to grow at a slower pace. According to USDA data, global oilseed meal imports, which stood at 107 million tons in the 2024/25 season, will reach approximately 110 million tons in the 2025/26 season. In the same season, the largest importers by country are expected to be the EU with 22.5 million tons, China with 9 million tons and Vietnam with 7.6 million tons. Argentina ranks first in terms of exports. According to USDA estimates, Argentina will export 31.2 million tons, Brazil 23.2 million tons, and the US 17.6 million tons of oilseed meal in the 2025/26 season.

A very large portion of global oilseed meal trade is in the form of soybean meal. According to USDA estimates, 78.6 million tons of soybean meal will be imported in the 2025/26 season. The EU will lead soybean meal imports with 17.6 million tons, followed by Vietnam with 6.6 million tons and Indonesia with 6.2 million tons. Argentina (30.1 million tons), Brazil (23.2 million tons) and the US (17.4 million tons) will account for the bulk of global soybean meal exports.

Rapeseed meal trade is quite limited compared to soybean meal. Rapeseed meal imports are estimated to reach approximately 10.2 million tons in the 2025/26 season. China is the largest importer in this product group, with 2.6 million tons. In terms of exports, Canada is the clear leader, with 5.5 million tons of rapeseed meal exports. India follows with 1.8 million tons.

International trade in other oilseeds and meal is quite low.

IMPACT OF SUPPLY AND DEMAND EXPECTATIONS

The 2025/26 season is notable for strong production and crushing volumes in the oilseed market. High production figures for key products such as soybeans, rapeseed and sunflower seeds appear poised to meet global protein and vegetable oil demand.

However, dynamics such as China’s changing import strategies, rapeseed trade tensions between Canada and China, geopolitical fragilities in the Black Sea region, and production uncertainties in South America due to weather conditions continue to be decisive in the direction of global oilseed trade.

In the feed sector, soybean, rapeseed and sunflower meal retain their importance as primary protein sources, while demand for alternative protein sources such as palm kernel meal is also increasing. In the vegetable oil market, the trio of palm oil, soybean oil and sunflower oil will continue to drive global demand.

References

1. Oilseeds: World Markets and Trade | USDA Foreign Agricultural Service

2. International Grains Council, Grain Market Report