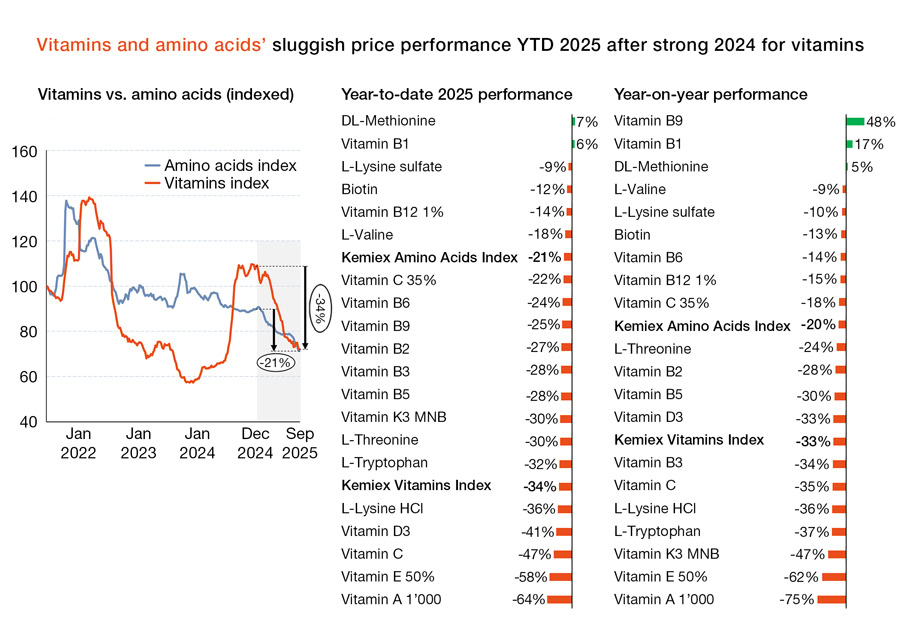

In 2025, prices for most vitamins, amino acids, and other feed additives fell sharply due to weak demand from the feed sector, amplified by trade and consumption uncertainties that drove hand-to-mouth purchasing and inventory drawdowns. While Methionine and Vitamin B1 prices held stable to firm year-on-year and year-to-date, Vitamins A and E saw steep declines from elevated levels caused by the BASF force majeure, fueled by expectations of production restarts and price normalization.

By Stefan Schmidinger, Chief Economist at Kemiex

Earnings reports for the second quarter and first half of 2025 highlight robust resilience and growth across most ingredients producers and sector participants, but outlooks were growing cautious, according to Kemiex’s latest Monthly Market Pulse report. Corporate growth was attributed to a mix of increased volumes and previously favorable prices for select vitamins and amino acids. Additives markets continue to show moderate momentum, even as fourth-quarter contraction intensifies and as key industry events such as VIV Nanjing and SPACE delivered few surprises. Companies cite risks from ever-changing tariff policy and uncertainty, anti-dumping cases, currency developments, and lackluster downstream demand.

BASF has lifted force majeure for multiple forms of Vitamin A, Vitamin E, and other products between June and September, enabling a phased reentry into its core animal and human nutrition markets expected from Q4.

In the wider downstream agri-food sector, animal diseases such as avian flu continue to spark volatility from temporary trade bans between countries. China is pressing forward with anti-dumping investigations into European Union pork imports, while summoning its top 25 domestic pig producers to curtail overproduction amid persistently weak prices.

Global freight rates have fallen for more than 14 consecutive weeks, though the pace of decline varies across trade lanes. China’s Golden Week in October could offer a brief reprieve, but persistent supply-demand imbalances are set to weigh on prices in the medium term as new vessel deliveries and limited capacity controls outstrip demand. No short-term resolution of the Suez Canal passage is expected.

ADDITIVES PRICES EASING, REBOUND RISK RISING

In 2025, prices for most vitamins, amino acids, and other feed additives fell sharply due to weak demand from the feed sector, amplified by trade and consumption uncertainties that drove hand-to-mouth purchasing and inventory drawdowns. While Methionine and Vitamin B1 prices held stable to firm year-on-year and year-to-date, Vitamins A and E saw steep declines from elevated levels caused by the BASF force majeure, fueled by expectations of production restarts and price normalization. From January to late September, the Kemiex Vitamins Index plummeted -34%, and the Kemiex Amino Acids Index dropped -21% (Figure 1).

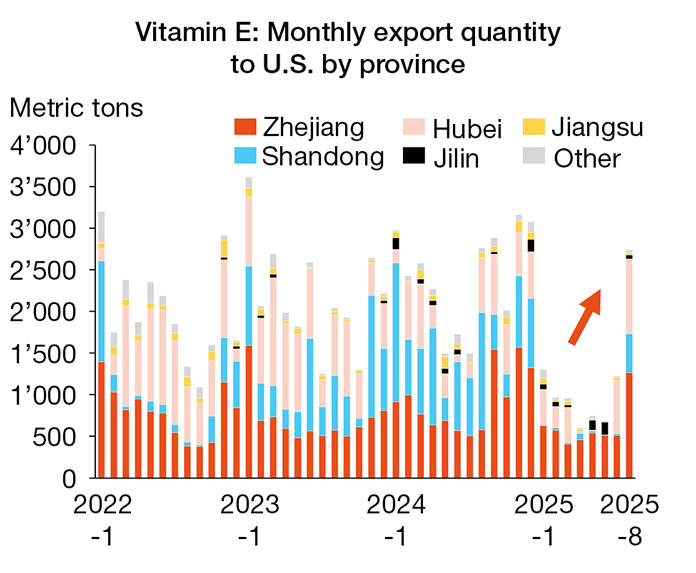

In August 2025, China’s exports remained largely subdued, however, Vitamin E shipments soared to a record 11,000 metric tons, the highest monthly volume ever recorded. The critical China-to-U.S. trade route for Vitamin E rebounded sharply after seven months of very low activity, reducing the year-to-date shortfall compared to 2024 to a -48% decline, or 8,500 metric tons, driven by Shandong, Zhejiang and Hubei provinces (Figure 2).

The European Union has approved Vitamin B2 from Chifeng, Chromium DL-Methionine from Zinpro, L-Arginine from CJ, and several other feed additives for market entry. Multiple companies announced upgrades to their production projects, including Brother, Garden, Tatneft, Golden Corn, Furui Biopharm, and others. Meanwhile, methionine producer Unisplendour is reportedly undergoing asset restructuring to shift its control and governance structure.

CURRENCY RATES IN SPOTLIGHT

Over recent months, significant fluctuations in key trade currencies for feed and other raw materials have impacted global markets. The USD Index, which tracks the U.S. dollar against a basket of major currencies, has fallen approximately -10% year-to-date in 2025, lingering at weaker levels comparable to those observed in February 2022.

In mid-September 2025, the Federal Reserve executed a moderate 25-basis-point interest rate cut, navigating softening labor markets and cooling inflation while resisting political demands for more aggressive action for now. The European Central Bank is anticipated adopting a cautious approach to further rate reductions, constrained by ongoing inflationary pressures. China’s monetary policy currently shows no signs of significant interventions or Yuan devaluation despite its economic woes.

The EUR/USD currency pair climbed to a range of 1.17–1.19, reflecting a weaker U.S. dollar and a +15% year-to-date gain, while the USD/CNY pair hovered around 7.10, down a few percentage points from the start of 2025 with some banks expecting a range of 7.00-7.08 near-term.

A depreciating U.S. dollar increases the cost of feed additive imports from major suppliers like China and Europe when priced in USD. In Europe, a euro that has strengthened by over +10% year-to-date against both the dollar and Chinese yuan makes imports more affordable, but this puts European brands at a disadvantage as China’s USD-denominated export prices translate to lower euro values. European producers and exporters are somewhat grappling with foreign exchange challenges due to misaligned revenue and cost structures.

DSM-FIRMENICH ANH DEAL UPDATE

dsm-firmenich’s Animal Health & Nutrition (ANH) divestiture announcement is now expected in Q4, from October onwards, following extended and complex due diligence but still broadly in line with the H2 timeline. Finalizing the ANH carve-out is an awaited milestone, providing clarity for both the remaining group and the divested ANH business for investors, employees and sector participants alike.

Meanwhile, August and September sales reportedly softened, driven by cautious inventory management by U.S. multinationals and FX headwinds that could impact Q3 by EUR 30 million or more, while key vitamin prices continued to decline. Growth in Taste, Texture & Health (TTH) is being supported by revenue synergies, alongside new capacity investments, including the near-complete Bovaer facility and a new pet food plant.

U.S. CONTINUES TO SHAPE GLOBAL MACRO LANDSCAPE

Global trade remains clouded by uncertainty amid bold and unpredictable U.S. policy shifts, with negotiations stalled across multiple fronts and no resolution in sight. The latest Trump-Xi talks produced no breakthroughs, pushing expectations to a potential in-person meeting at the APEC summit in late October or early November. Early signals from U.S. negotiators indicate that a meaningful trade deal may even not materialize until 2026. The ongoing Section 301 investigation into Brazil is followed closely, as it could affect this major agri-food trade.

In June, the U.S. Environmental Protection Agency (EPA) proposed new Renewable Volume Obligations (RVOs) under the Renewable Fuel Standard (RFS), projecting a 67% increase in biomass-diesel volumes from 3.35 to 5.61 billion gallons for 2025-26. The move has initially supported soybean and oil prices, though the resulting surge in soybean meal output from crushing needs to find outlets in the domestic and export market, weighing on soy meal and animal feed prices, and consequentially risking lower amino acids inclusion.

Meanwhile, U.S. soybean sales for the 2025/26 marketing year trailed 40% below the long-run average of 13mmt by late August, with China making no purchases—a repeat of 2019 trade-war patterns. Brazil and Argentina have stepped in to fill China’s soybean demand, while U.S. corn yields are set to hit record levels; U.S. corn exports remain robust, driven by growth in Mexico, Japan, Korea, and Colombia despite the absence of Chinese purchases.

Lengthened 2025’s uncertainties and trade barriers have pressured sentiment, prices, production and inventories, and feed additives markets may brace for sudden and heightened volatility from here into H1 2026.