Head of Feed Sector

Agricultural Industries Confederation (AIC)

Since the EU exit on 31 January 2020, the UK animal feed industry is managing the implications of departure from the trade bloc including, those for trade, regulation, and the ambition of the UK Government to improve food security.

TRADE

The UK industry sources 16mt of raw materials annually, with 54% from home-grown origins and the remainder globally. This exposes the industry to geopolitical shocks such as Covid, the war in Ukraine, Suez supply challenges, and now a looming global trade war.

It would be fair to conclude that the UK animal feed industry has yet to see benefits from the EU exit. However, independent of the EU, the UK may navigate a competitive advantage, with US tariff proposals and EU countermeasures being a prime example.

The initial US tariff proposal for EU goods was 20%, whilst only 10% for UK goods. In response, the EU proposed countermeasures of 25% on various US food and feed goods. The UK has not imposed any tariffs to date, but the Government is consulting on the issue.

The UK imports various feed materials and additives from the US, either directly or via the EU. These include maize, soya beans and meal, beet pulp, beet molasses, distiller’s dried grains with solubles (DDGs), corn gluten, a range of feed additives, and amino acids.

Another example of an independent UK trade policy that benefits the feed industry is the decision not to place any anti-dumping measures on Chinese lysine imports. The EU provisional measures were set out in Implementing Regulation (EU) 2025/74 on 13 January 2025 and, if imposed, will have considerable economic implications for the EU industry.

However, Northern Ireland feed businesses importing Chinese lysine will be subject to EU measures, though these may be reversed under the Windsor Framework.

The Agricultural Industries Confederation (AIC), representing the interests of the UK feed industry, is engaged in discussions with the UK Government on tariffs and will be seeking a positive outcome for Members.

While trade policies are crucial, another significant area of focus for the UK feed industry is the regulatory landscape, particularly the opportunity to negotiate a UK/EU Sanitary and Phytosanitary (SPS) Veterinary Agreement.

UK/EU SPS VETERINARY AGREEMENT

AIC has engaged in separate discussions with the Department for Environment, Food and Rural Affairs (Defra) over the Government’s ambition to negotiate an EU-SPS veterinary agreement. The Government has now begun the work of negotiating such an agreement with the EU, a policy shift that could benefit the entire agri-food supply chain in the UK. Since the Government took office, AIC has been working closely with ministers and civil servants as they engage in these negotiations to help foster a beneficial outcome for Members, to remove unnecessary barriers to trade between the UK and EU. Amongst such challenges, one cannot overlook the complexities that have arisen from trade between Great Britain and Northern Ireland in SPS matters. On 19 May, a high-level EU-UK summit will take place in London, and this will form part of the discussions.

REGULATION

Regulation is another area where UK policy proposals are leading to greater divergence from EU feed regulations. Simplifying the regulated products regime will benefit feed businesses. The UK Food Standards Agency (FSA) has proposed removing the need for 10-year renewals for feed additives, genetically modified organisms (GMOs), and smoke flavourings. They also suggest publishing authorisations after a ministerial decision, rather than prescribing them in legislation.

These proposals are welcomed by industry and will help ensure speedier approvals for new feed additives and GMOs and remove the cost of preparing and submitting dossiers for renewals.

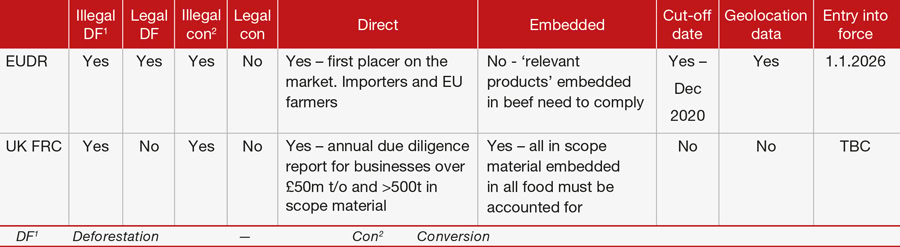

Proposed deforestation regulations in the EU and UK have occupied much feed industry resource and, in the UK, the focus has been on identifying the differences between the EU Deforestation Regulation (EUDR) and the UK Forest Risk Commodities Regulation (UKFRC).

The table below highlights the main differences:

Again, the UK deforestation regulation proposals appear pragmatic, and the industry supports the principle of deforestation-free supply chains. AIC has engaged in discussions with food and feed supply chain partners to highlight the extra compliance costs both sets of regulations will bring. It is important to note that Northern Ireland businesses might need to follow both UKFRC and EUDR rules.

Again, the UK deforestation regulation proposals appear pragmatic, and the industry supports the principle of deforestation-free supply chains. AIC has engaged in discussions with food and feed supply chain partners to highlight the extra compliance costs both sets of regulations will bring. It is important to note that Northern Ireland businesses might need to follow both UKFRC and EUDR rules.

A further regulatory proposal in the UK is the Precision Breeding (PB) Act, which regulates technologies such as gene-editing in plants and animals, presents an opportunity for the UK feed industry. In February 2025, UK Ministers announced that secondary legislation to implement the Precision Breeding Act for plants would be laid in Parliament. The necessary secondary legislation is expected to pass through Parliament and will allow FSA and Defra to receive applications for Precision Bred Organisms (PBOs) in England. AIC will represent the industry’s interests in the Government’s Precision Breeding Working Group, to ensure consistency of PB legislation across the UK, noting that similar legislation has now taken a step further forwards in the EU.

While regulatory changes are essential for industry growth, ensuring food security remains a priority for the UK Government, especially in responses to recent global challenges.

UK FOOD SECURITY

The UK Government has published a Food Security Report which identifies the challenges to the UK food supply chain resulting from major shocks such as:

• Societal responses to the COVID-19 pandemic caused fluctuations in supply chains due to government measures and economic stimulus,

• Russia’s invasion of Ukraine in February 2022 disrupted energy and grain supplies, leading to higher food prices and impacting UK food security,

• Conflict in the Middle East altered supply routes, showing the global trade system’s adaptability,

• Extreme weather conditions, exacerbated by climate change, caused further localized food chain disruptions.

The report serves as an independent evidence base to inform users rather than a policy or strategy. In practice, this means that it provides the Government, Parliament, food chain stakeholders, and the wider public with the data and analysis needed to monitor UK food security and develop effective responses to issues.

The UK feed industry is developing a risk register for feed materials and additives to inform discussions around food security issues – after all, food security depends to some extent on feed security.